{kind=link}

Steady enchancment in India; geopolitics weigh on RM prices and international enterprise

* We interacted with Mr. Ankush Jain, CFO of Dabur India (Dabur) to debate business developments, the corporate’s progress outlook throughout verticals, international volatility, and its longterm methods. Amid provide chain disruptions, Dabur’s worldwide enterprise has taken a success (MENA accounts for 8% of consol. gross sales), which we imagine may weigh on Dabur’s near-term consolidated efficiency.

* The firm’s India enterprise continues to witness sequential enchancment in demand developments. Domestic enterprise is predicted to point out higher YoY progress in 4QFY26 as in comparison with 3QFY26. Global uncertainties haven’t impacted consumption as of now. The firm has not taken any worth hikes but, although it continues to observe commodity worth actions carefully. Looking forward, administration expects FY27 progress to be largely led by quantity progress, topic to commodity volatility.

* Category developments stay broadly wholesome throughout the portfolio. Dabur is seeing wholesome progress momentum in oral care (~16% market share) and hair care (robust doubledigit progress) segments. Healthcare demand stays comparatively muted, however there may be sequential enchancment. In residence care, progress is predicted to maneuver towards excessive single digits, aided partly by a positive base. The meals portfolio is rising steadily, whereas drinks are anticipated to develop in low single digits within the close to time period. A good outlook for drinks in FY27 is properly supported by a weak base.

* On profitability, administration expects regular margins within the close to time period. The firm could take into account worth hikes mid-April onward if enter prices stay elevated. Packaging materials (PM) prices account for ~15% of gross sales and 25-30% of whole uncooked materials (RM) prices. EBITDA margins are anticipated to broaden YoY within the close to time period.

* Quick commerce (QC) continues to achieve traction and now contributes 4-5% of India income (50% of ecomm), accounting for roughly half of whole ecommerce gross sales. The progress trajectory stays robust (30-40%) in QC channel.

* Dabur posted muted progress in FY25 (1.3%) and 9MFY26 (4%), with mid-single-digit progress anticipated in 4Q regardless of high-single-digit progress in India. Given its management transition from Mr. Mohit Malhotra to Mr. Herjit Bhalla, we are going to look ahead to any strategic precedence adjustments by the brand new CEO. Apparently, Mr. Malhotra will proceed to be a part of Dabur and will take care of M&A, technique and worldwide fronts.

* Domestic macro indicators are supporting a gradual consumption restoration, although persistent execution challenges hold us cautious. Factoring in near-term headwinds in Dabur’s worldwide markets, we trim our EPS estimates by 2-3% and keep Neutral with a TP of INR515 (40x Mar’28E EPS).

Geopolitical uncertainties to weigh on consol. efficiency in close to time period

* Dabur acknowledged that supply-chain disruption has emerged throughout key transport routes, significantly across the Red Sea and the Strait of Hormuz, affecting product motion within the GCC markets.

* Moreover, the corporate is seeing softened consumption developments within the area as residents stay indoors and the vacationer inhabitants has declined.

* From a income combine perspective, the MENA area contributes ~8% of Dabur’s consolidated income, whereas Turkey accounts for ~3-4%.

* While the corporate entered the quarter with robust momentum, the continued battle has led administration to reasonable progress expectations for worldwide enterprise.

* Given the rising headwinds, administration has lowered its near-term consolidated progress steering from excessive single digits to mid-single digits, largely reflecting the slowdown in worldwide markets.

India FMCG enterprise continues to see sequential enchancment

* Rural demand continued to outperform city demand. However, the ruralurban progress hole has narrowed to ~250bp from ~500bp earlier, indicating a gradual enchancment in city demand. The firm is seeing a restoration in city demand.

* Domestic FMCG progress stood at 6% in 3QFY26, which administration expects to enhance forward. Encouragingly, as per Dabur, the primary 10 days of March haven’t proven any materials slowdown in shopper demand.

* The firm has not carried out worth hikes presently however continues to observe commodity worth actions.

* Management expects progress in FY27 to be led by quantity, topic to commodity volatility.

Healthy progress throughout classes

* Oral Care: Dabur maintains a ~16% market share in oral care (No. 2 participant within the house), with family penetration of ~52-53%, implying each second family in India makes use of a Dabur oral care product. Management sees important headroom for additional market share beneficial properties.

* Hair Care: The phase is witnessing robust double-digit progress, supported by a structural shift in shopper desire from coconut oil towards perfumed hair oils, which additionally carry greater margins for the corporate. Coconut hair oil makes up 20-25% of its total hair oil combine.

* Healthcare: The class stays comparatively muted however is predicted to see gradual enchancment forward. Dabur indicated that choose over-the-counter (OTC) manufacturers like Pudinhara and Honitus are reportedly exhibiting sequential enchancment.

* Home Care: While the class had beforehand been seeing low single-digit progress, administration now expects it to achieve close to excessive single digits. That stated, the present enchancment is partly because of a positive base; within the earlier 12 months, there have been provide points in GT. The firm is continuous to see market share beneficial properties on this class.

* Foods & Beverages (F&B): The meals portfolio continues to develop at a wholesome tempo. In the close to time period, Dabur expects drinks to develop at a low single-digit fee, whereas the mixed F&B class is projected to develop at a mid-single digit fee. For FY27, administration anticipates a greater trajectory for F&B class, noting that the bottom is kind of favorable because of the poor summer season efficiency within the earlier 12 months. Management additional famous that the drinks portfolio ought to a minimum of develop in mid-single digits.

Dabur expects regular margins in close to time period

* Dabur has not elevated costs presently, as the corporate carries FG/RM stock, together with wholesome stock at commerce channel. However, administration indicated that worth hikes could also be thought of from mid-April onward if crude-linked enter prices stay elevated.

* PM prices account for ~15% of gross sales and 25-30% of whole RM prices. Earlier estimates assumed 2-2.5% RM-PM inflation (excl. coconut); therefore, the corporate was anticipating a restricted worth hike requirement in FY27. However, given present geopolitical volatility, there could possibly be a change within the worth hike outlook.

* EBITDA margin is predicted to enhance within the close to time period; nonetheless, commodity volatility can change the outlook for FY27.

Quick commerce makes up 4-5% of India enterprise gross sales

* QC continues to achieve traction and presently contributes 4-5% of Dabur’s India income. It now accounts for ~50% of whole e-commerce gross sales.

* Management highlighted that QC and e-commerce channels usually skew towards premium product codecs (bottles, bigger packs) in contrast with common commerce, which is essentially pushed by sachets.

* Dabur continues to deal with strengthening its distribution attain. It expanded its whole attain (city + rural) to over 8.5m shops, making it the second-most distributed FMCG firm in India.

Valuation and consider

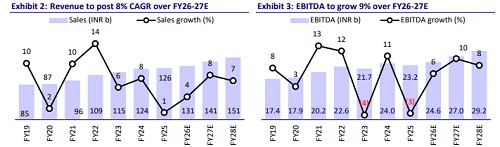

* The firm has been reporting muted gross sales progress over the previous two years. After delivering 1.3% progress in FY25, income progress improved modestly to 4% in 9MFY26. Management is guiding for mid-single-digit progress in close to time period (high-single-digit progress for India).

* Considering management adjustments from Mohit Malhotra to Herjit Bhalla, we are going to look ahead to any strategic precedence adjustments by the brand new CEO. Apparently, Mr. Malhotra will proceed to be a part of Dabur and will take care of M&A, technique and worldwide fronts.

* We stay optimistic on consumption restoration, supported by bettering home macros, however cautious on international uncertainties. However, Dabur’s constant weak execution, regardless of macros turning optimistic, is regarding, in our view. The inventory has remained range-bound over the past 5 years. Factoring near-term headwinds in Dabur’s worldwide markets, we trim our EPS estimates by 2-3% and keep Neutral with a TP of INR515 (40x Mar’28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration quantity is INH00000041