{kind=link}

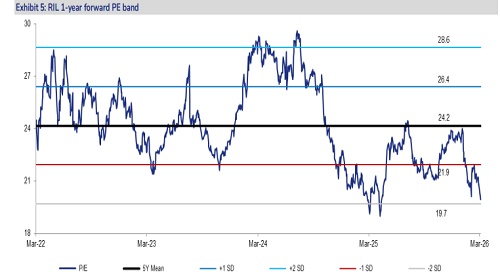

We consider the current correction in RIL’s share value is overdone (4% this week and eight% within the final 1 month after rise in Middle East tensions) because it received’t be negatively impacted by the current spike in crude and LNG costs. Instead, RIL might see near-term advantages on account of: a) soar in diesel crack on account of provide disruption threat; and b) seemingly rise in petchem margin (as petchem product costs are more likely to rise together with crude value whereas its feedstock price is unlikely to rise a lot because it has restricted dependency on crude-linked naphtha). The correction in RIL appears largely on account of FII-related promoting (FII holding at 21.1% at end-Dec’25 versus peak of 28.3% at end-Mar’21). At CMP, RIL is buying and selling close to our bear-case valuation of ~INR 1,275/share – exhibit 3. We reiterate BUY (unchanged TP of INR 1,730) on snug valuations after the current correction, as share value adequately elements concern round near-term weak spot in retail enterprise EBITDA progress on account of ramp-up within the fast commerce enterprise. However, it’s not discounting 15-16% EBITDA-compounding story in Digital enterprise over the subsequent 2-3 years pushed by 10-11% ARPU CAGR; therefore we count on 14-16% EPS CAGR for RIL over the subsequent 3-5 years. Key triggers are Jio’s IPO within the subsequent few months (assuming SEBI norms for giant IPOs are notified within the subsequent few weeks) and certain telecom tariff hike publish that. At CMP, the inventory is buying and selling at FY28E P/E of 16.8x (3-year common 23.9x) and FY28E EV/EBITDA of 8.2x (3-year common 11.9x).

* Spike in crude/LNG value doesn’t hit RIL’s O2C enterprise earnings; as a substitute RIL to see nearterm profit on account of soar in diesel crack and certain rise in petchem margin: We consider the current correction in RIL’s share value is overdone (4% this week and eight% in final 1 month after escalation in Middle East tensions) because it doesn’t get negatively impacted because of the current spike in crude and LNG costs. Instead, RIL advantages on account of soar in diesel cracks to USD 35-42/bbl within the final 2 days (~USD20/bbl earlier) because the diesel yield for RIL’s refinery is a excessive 40-50%; assuming diesel crack sustains at ~USD30/bbl, RIL’s GRM might rise by USD 4-5/bbl. Every USD 1/bbl rise in RIL’s GRM on an annualised foundation ends in a rise in its annual EBITDA by INR 45bn or 2.2% and enhance in valuation by INR 29/share of 1.7%. However, we agree this abnormally excessive diesel crack will not be sustainable; additionally, there may very well be a threat of the federal government taking it away through windfall tax (much like motion taken publish Russia-Ukraine disaster when the federal government capped diesel/petrol crack at ~USD20/bbl and took margin past that through windfall tax). Further, RIL additionally advantages on account of seemingly rise in its petchem margin as petchem product costs are more likely to rise together with crude value, whereas its petchem feedstock price is unlikely to rise a lot because it has restricted dependency on crude-linked naphtha. RIL’s petchem feedstock breakdown is roughly: i) 25% ethane; ii) 50% off-gases and iii) and solely 25% crude-linked naphtha

* Correction in RIL overdone; at the moment buying and selling close to our bear-case valuation: We consider the correction in RIL is essentially on account of FII-related promoting given RIL is a big liquid holding for FIIs (FII holding of 21.1% at end-Dec’25 versus peak of 28.3% at end-Mar’21). At CMP, RIL is buying and selling close to our bear-case valuation of ~INR 1,275/share (exhibit 3) which relies on: a) 20x FY28E EV/EBITDA a number of for the retail enterprise (25x within the base case) and 15% minimize in FY28E retail EBITDA estimate to account for near-term weak spot in retail enterprise EBITDA progress on account of ramp-up within the fast commerce enterprise; b) 11x FY28E EV/EBITDA a number of for the telecom enterprise (12.6x within the base case) – at CMP, Bharti India enterprise is buying and selling at 9.5-10x FY28E EV/EBITDA; c) New Energy enterprise at 1x of INR750bn funding (2x in base case); d) 6.5x FY28E EV/EBITDA for O2C enterprise (7.5x within the base case) and 10% decrease EBITDA factoring in threat of some affect on refinery throughput on account of some scarcity of crude availability;

* Reiterate BUY on snug valuations, and as we count on robust 14-16% EPS CAGR over the subsequent 3-5 years significantly pushed by each shopper companies: We reiterate BUY (unchanged TP of INR 1,730) on snug valuations after the current correction, as share value adequately elements concern round near-term weak spot in retail enterprise EBITDA progress on account of ramp-up within the fast commerce enterprise. However, it’s not discounting 15-16% EBITDA-compounding story in Digital enterprise over the subsequent 2-3 years pushed by 10-11% ARPU CAGR; therefore we count on 14-16% EPS CAGR for RIL over the subsequent 3-5 years. Key triggers are Jio’s IPO within the subsequent few months (assuming SEBI norms for giant IPOs are notified within the subsequent few weeks) and certain telecom tariff hike publish that. Further we count on its web debt to say no progressively as a result of capex is not going to solely average (INR 1.2tn-1.4tn p.a. versus INR 2.3tn in FY23 and INR 1.3tn in FY24 and FY25) however, importantly, even be totally funded by a gradual enhance in inside money technology. RIL’s steerage on retaining reported web debt to EBITDA beneath 1x (0.6x at end3QFY26) additionally offers consolation. At CMP, RIL is buying and selling close to our bear-case valuation of ~INR 1,275/share. At CMP, the inventory is buying and selling at FY28E P/E of 16.8x (3-year common: 23.9x) and FY28E EV/EBITDA of 8.2x (3-year common: 11.9x). Key dangers: a) weak subs addition and restricted ARPU hike; b) sustained muted progress within the retail enterprise; and c) subdued O2C margins on account of macro issues.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361