Reassessing Amazon.com (AMZN) After 121% Three Year Rally And Recent Share Price Pullback

After 121% Three Year Rally And Recent Share Price Pullback")

- If you might be questioning whether or not Amazon.com remains to be an affordable entry at round US$209.97, the important thing query is whether or not the present worth displays its underlying enterprise worth.

- After a 121.3% return over 3 years however a 13.6% decline over the previous 30 days and a 7.3% decline 12 months to this point, some buyers are reassessing each the expansion potential and the extent of threat they’re taking over with Amazon.com.

- Recent information move round Amazon.com has continued to concentrate on its position as a big e commerce and cloud providers supplier, in addition to its affect in areas like digital promoting and logistics. These themes typically body how buyers interpret shorter time period share worth strikes, particularly when sentiment shifts between progress and profitability priorities.

- Right now Amazon.com has a valuation rating of 5/6, primarily based on the way it screens throughout six completely different undervaluation checks. Next, we are going to take a look at what numerous valuation strategies point out, earlier than ending with a broader approach to consider what this rating actually means for long run buyers.

Approach 1: Amazon.com Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, mannequin tasks an organization’s future money flows after which reductions these projections again to right this moment, to estimate what the entire enterprise is likely to be value in present {dollars}.

For Amazon.com, the mannequin here’s a 2 Stage Free Cash Flow to Equity method that makes use of the corporate’s final twelve months free money move of about $40.11b as a place to begin. Analysts present money move estimates for the following few years, and Simply Wall St then extends these projections additional. In this case, the projections attain a free money move determine of $173.80b in 2030, with intermediate years starting from a projected money outflow in 2026 by to steadily bigger inflows by 2035.

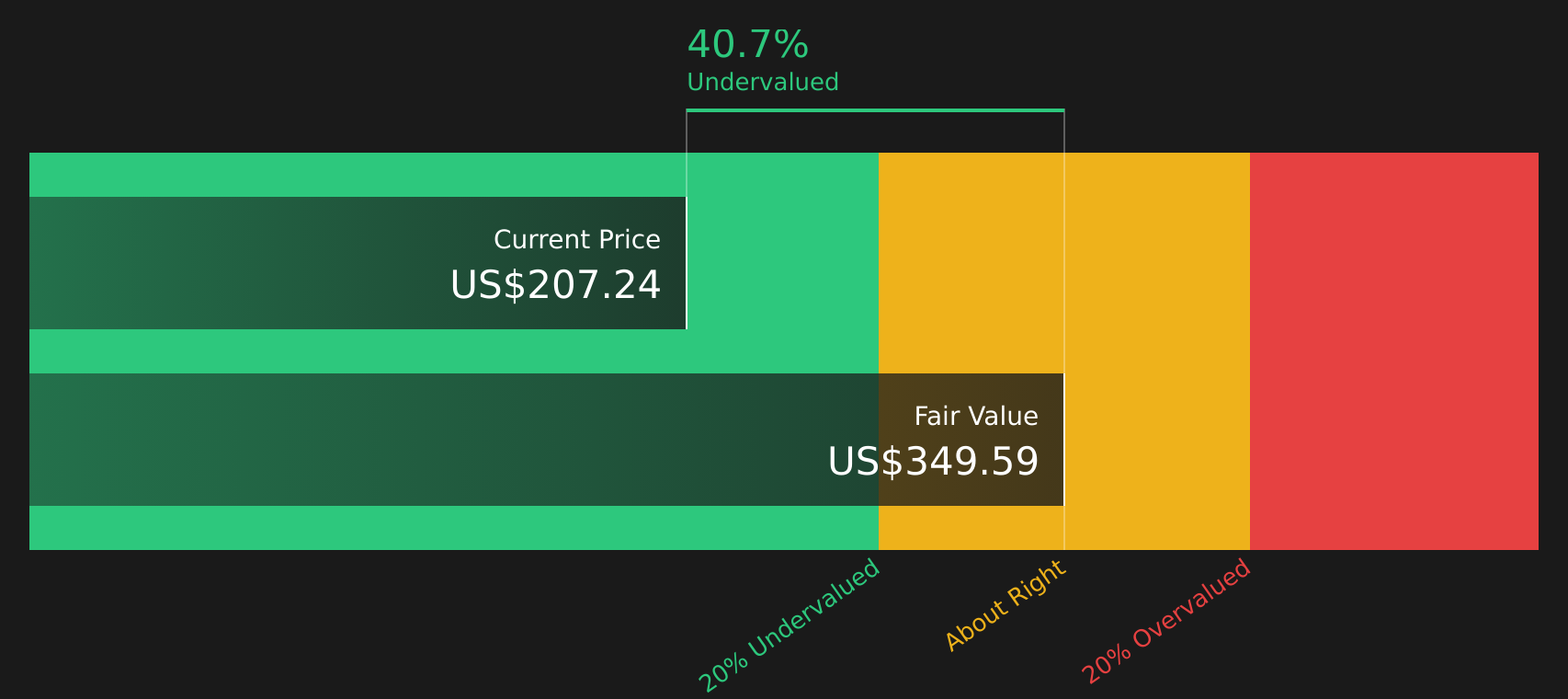

When all of these projected money flows are discounted again to right this moment, the mannequin arrives at an estimated intrinsic worth of about $361.52 per share. Compared with the present share worth of roughly $209.97, this implies the inventory is buying and selling at a 41.9% low cost to that DCF estimate, indicating a significant margin between worth and modeled worth.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) evaluation suggests Amazon.com is undervalued by 41.9%. Track this in your watchlist or portfolio, or uncover 46 more high quality undervalued stocks.

Approach 2: Amazon.com Price vs Earnings

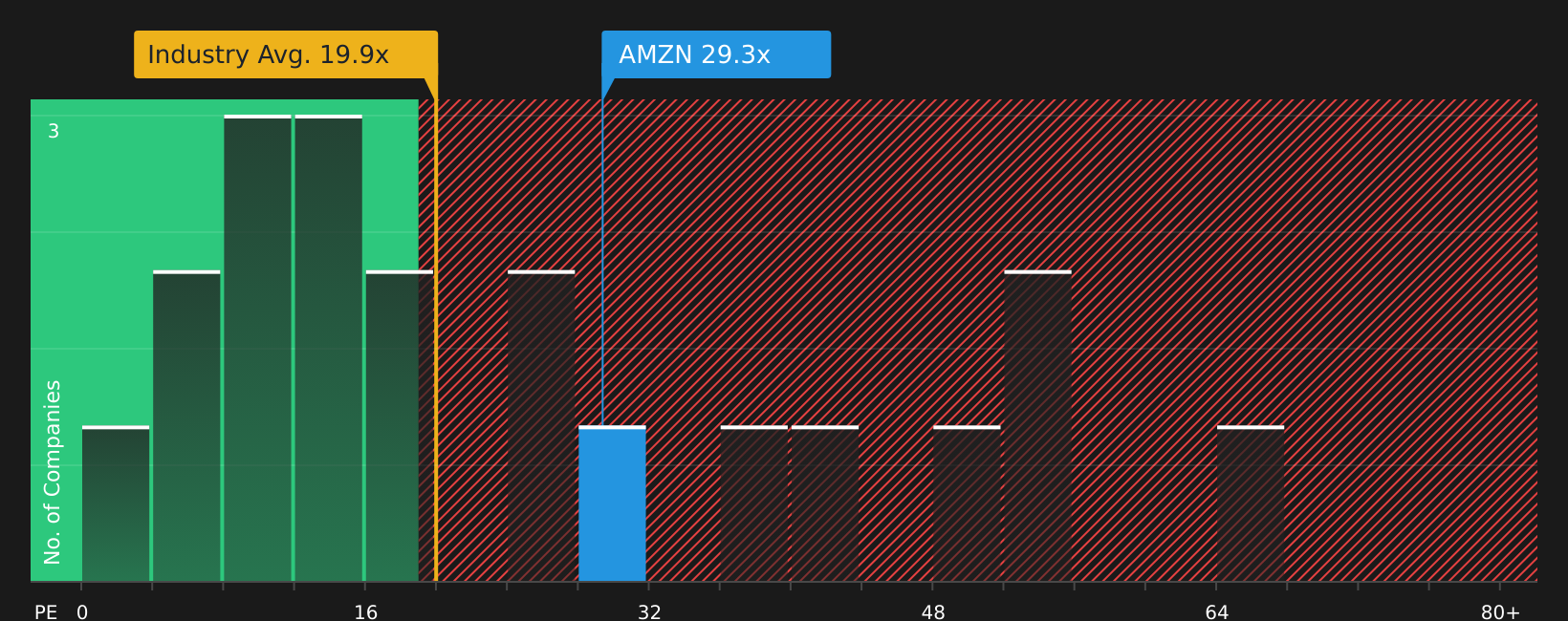

For a worthwhile firm like Amazon.com, the P/E ratio is a helpful solution to join what you pay right this moment with the earnings the enterprise is already producing. It helps you see what number of {dollars} of worth you might be paying for every greenback of present earnings.

What counts as a “normal” or “fair” P/E is determined by how shortly earnings are anticipated to develop and the way dangerous these earnings are. Higher progress or decrease perceived threat can justify the next P/E, whereas slower progress or greater uncertainty can level to a decrease one.

Amazon.com at present trades on a P/E of 29.02x. That is near its peer common of 29.34x and above the Multiline Retail trade common of 20.25x. Simply Wall St’s Fair Ratio for Amazon.com is 41.55x, which is a proprietary estimate of what the P/E is likely to be given components like earnings progress, revenue margins, trade, market cap and threat profile. Because it blends these components into one quantity, the Fair Ratio might be extra tailor-made than a easy comparability with friends or the broad trade.

Comparing the Fair Ratio of 41.55x with the present P/E of 29.02x suggests Amazon.com is buying and selling beneath that model-based estimate.

Result: UNDERVALUED

P/E ratios inform one story, however what if the true alternative lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Amazon.com Narrative

Earlier we talked about that there’s an excellent higher solution to perceive valuation, so allow us to introduce you to Narratives, a easy approach so that you can connect a transparent story about Amazon.com to the numbers you care about, like honest worth estimates and assumptions for future income, earnings and margins.

A Narrative on Simply Wall St hyperlinks three items collectively: your view of Amazon.com as a enterprise, a monetary forecast constructed from inputs reminiscent of progress, revenue margins and low cost price, and a ensuing honest worth that you may evaluate instantly with right this moment’s share worth to border purchase or promote choices in a extra structured approach.

These Narratives can be found on the Simply Wall St Community web page, are up to date mechanically when new data reminiscent of information or earnings is added to the platform, and are designed so you’ll be able to regulate a number of inputs somewhat than construct a full mannequin from scratch.

Looking at present Amazon.com Narratives illustrates the vary of views. One group member at present anchors on a good worth close to US$135 per share, whereas one other is nearer to US$500 per share. That unfold displays very completely different tales about how shortly AWS, promoting and automation could translate into margins and money flows somewhat than a single “right” quantity.

For Amazon.com nonetheless we are going to make it very easy for you with previews of two main Amazon.com Narratives:

Together they present how buyers can take a look at the identical enterprise fundamentals and attain very completely different conclusions about what the inventory is value right this moment.

Fair worth on this bullish Narrative: US$222.55 per share

Implied pricing hole vs final shut of US$209.97: round 6% beneath the Narrative honest worth

Revenue progress assumption: 15.19%

- Sees Amazon’s true earnings energy coming from third social gathering sellers, promoting and AWS, with present accounting and heavy reinvestment masking underlying profitability.

- Assumes continued reinvestment into achievement, cloud and promoting retains free money move muted within the close to time period whereas working money move and margins construct behind the scenes.

- Places extra weight on the lengthy runway for ecommerce, cloud migration and on-platform promoting, whereas recognising regulatory and macro dangers that would sluggish the trail to these money flows.

Fair worth on this extra cautious Narrative: US$151.21 per share

Implied pricing hole vs final shut of US$209.97: round 39% above the Narrative honest worth

Revenue progress assumption: 7.2%

- Focuses on Amazon’s dimension and present market share, arguing that the core retail enterprise could have much less room to develop and requires heavy ongoing capital funding to maintain progress.

- Assumes AWS and promoting stay vital revenue drivers however develop from a big base, whereas retail, commerce frictions and competitors from gamers like Walmart restrict how briskly the group can scale.

- Highlights points reminiscent of inventory primarily based compensation, capital depth and rising competitors, and builds in additional conservative expectations for long run margins and returns on capital.

Both Narratives use detailed phase stage assumptions and money move considering; they only weigh the identical information in another way. If you need to see how the group is framing these tales and the place your personal view suits in, Curious how numbers become stories that shape markets? Explore Community Narratives.

Do you assume there’s extra to the story for Amazon.com? Head over to our Community to see what others are saying!

This article by Simply Wall St is common in nature. We present commentary primarily based on historic information

and analyst forecasts solely utilizing an unbiased methodology and our articles will not be supposed to be monetary recommendation. It doesn’t represent a advice to purchase or promote any inventory, and doesn’t take account of your goals, or your

monetary scenario. We intention to convey you long-term targeted evaluation pushed by basic information.

Note that our evaluation could not issue within the newest price-sensitive firm bulletins or qualitative materials.

Simply Wall St has no place in any shares talked about.

New: Manage All Your Stock Portfolios in One Place

We’ve created the final portfolio companion for inventory buyers, and it is free.

• Connect an infinite variety of Portfolios and see your whole in a single forex

• Be alerted to new Warning Signs or Risks through electronic mail or cellular

• Track the Fair Value of your shares

Have suggestions on this text? Concerned concerning the content material? Get in touch with us instantly. Alternatively, electronic mail editorial-team@simplywallst.com